settlement for student loans

Are you burdened by the weight of your student loans? Feeling overwhelmed by the constant pressure to make monthly payments? You're not alone. Many individuals find themselves struggling to repay their student loans, often resulting in financial distress and a negative impact on their credit score. However, there is hope. Through the process of settlement, you may be able to find relief and achieve financial freedom.

In this comprehensive guide, we will delve into the topic of settlement for student loans, exploring the various options available to borrowers and the potential benefits they offer. Whether you're facing high interest rates, unaffordable monthly payments, or simply want to explore alternatives to traditional repayment plans, this article will provide you with the information you need to make an informed decision.

Understanding Student Loan Settlement

Student loan settlement is a process that allows borrowers to negotiate with their lenders to reach an agreement on a reduced payoff amount. Unlike traditional repayment plans, where borrowers are required to repay the full amount borrowed plus interest, settlement offers a chance to settle the debt for less than the total owed. This option is typically pursued by borrowers who are facing extreme financial hardship and are unable to meet their monthly payment obligations.

Eligibility Criteria

Not all borrowers are eligible for student loan settlement. Lenders typically require borrowers to demonstrate severe financial distress, such as unemployment, a significant reduction in income, or a prolonged period of financial hardship. Additionally, borrowers must usually be in default on their loans or be at risk of defaulting in the near future.

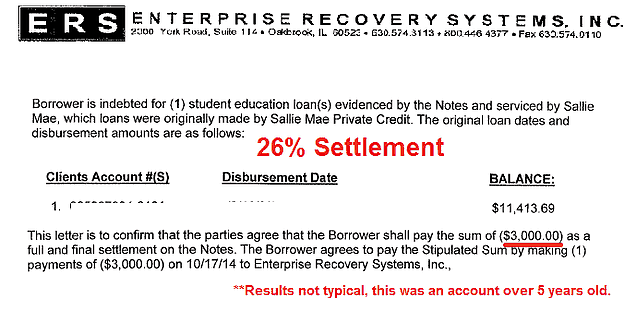

The Settlement Process

The process of settling student loans begins with contacting your lenders to express your financial hardship and discuss the possibility of a settlement. It is important to be prepared with documentation and evidence of your financial situation, as lenders will require proof of your inability to repay the loan in full. Once negotiations begin, lenders may offer a reduced payoff amount, which can be paid in a lump sum or through a structured repayment plan.

Consequences of Settlement

While student loan settlement can provide relief for borrowers in financial distress, it is important to be aware of the potential consequences. Settling a loan may result in a negative impact on your credit score, as it indicates that you were unable to fulfill your original repayment agreement. Additionally, the forgiven portion of the loan may be considered taxable income, potentially leading to a tax liability. However, these consequences may be outweighed by the benefits of settling the loan, such as avoiding bankruptcy or achieving financial stability.

Negotiating with Lenders

When negotiating a settlement with your lenders, it is essential to approach the process strategically to maximize your chances of success. Here are some effective strategies to consider:

1. Assess Your Financial Situation

Before entering into negotiations, take a thorough look at your financial situation. Calculate your total debt, income, and expenses to determine how much you can realistically afford to pay. This information will help you present a compelling case to your lenders.

2. Research the Market

Understanding the current market conditions and the typical settlement amounts for student loans can give you an advantage during negotiations. Research and gather information on recent settlements to support your case and negotiate more effectively.

3. Prepare Documentation

Gather all the necessary documentation to support your financial hardship. This may include bank statements, pay stubs, tax returns, medical bills, or any other evidence that demonstrates your inability to repay the loan in full. Having this documentation ready will strengthen your negotiating position.

4. Craft a Persuasive Argument

When negotiating with your lenders, present a clear and persuasive argument for why a settlement is the best option for both parties. Highlight the financial hardship you are facing, the potential benefits of a settlement, and your commitment to resolving the debt.

5. Be Persistent and Patient

Negotiating a settlement can be a lengthy process, so it's important to remain persistent and patient throughout. Be prepared for multiple rounds of negotiations and be open to compromise. Remember, lenders are often willing to negotiate if it means they can recover at least a portion of the loan.

Pros and Cons of Student Loan Settlement

Before opting for a student loan settlement, it is crucial to consider the advantages and disadvantages. Here are some pros and cons to help inform your decision:

Pros

1. Debt Reduction: Settling your student loans allows you to significantly reduce the amount you owe, providing immediate financial relief.

2. Avoiding Bankruptcy: By settling your loans, you can avoid the drastic step of filing for bankruptcy, which has long-lasting negative effects on your creditworthiness.

3. Repayment Flexibility: Through settlement, you may have the option to negotiate a structured repayment plan that better suits your financial capabilities.

4. Potential Savings: Settling your loans can save you money in the long run, as you won't have to pay the full amount plus accumulated interest.

Cons

1. Credit Score Impact: Settling your student loans can have a negative impact on your credit score, making it more challenging to obtain credit in the future.

2. Tax Implications: The forgiven portion of your loan may be considered taxable income, potentially resulting in a tax liability.

3. Limited Eligibility: Not all borrowers are eligible for settlement, and lenders may require specific criteria to be met before considering a settlement offer.

4. Potential Collection Efforts: In some cases, lenders may pursue collection efforts even after a settlement agreement is reached, such as garnishing wages or seizing assets.

Exploring Loan Forgiveness Programs

Loan forgiveness programs offer an alternative to settlement for borrowers struggling with their student loans. These programs, often sponsored by the government, provide relief by forgiving a portion or even the entire outstanding balance of the loan. Here are some popular loan forgiveness programs to consider:

Public Service Loan Forgiveness (PSLF)

The PSLF program is designed for borrowers who work full-time for a qualifying public service or non-profit organization. After making 120 qualifying payments, the remaining balance of the loan may be forgiven.

Teacher Loan Forgiveness

This program is specifically tailored for teachers serving in low-income schools or educational service agencies. Eligible teachers can receive loan forgiveness of up to $17,500 after meeting certain criteria.

Income-Driven Repayment Plan Forgiveness

Income-driven repayment plans, such as Income-Based Repayment (IBR) or Pay As You Earn (PAYE), offer forgiveness of the remaining loan balance after a certain number of qualifying payments. The forgiveness amount varies depending on the specific plan.

Perkins Loan Cancellation

Borrowers with Federal Perkins Loans may be eligible for cancellation of their loan if they work in certain professions, such as teaching, nursing, or serving in the military.

Rehabilitation vs. Settlement

When facing difficulty in repaying your student loans, you may have the option to choose between loan rehabilitation and settlement. While both options provide relief, they differ in their approach and potential impact. Here's a comparison to help you decide:

Loan Rehabilitation

Loan rehabilitation involves entering into an agreement with your lender to make a series of affordable payments over a designated period, typically nine months. Successful completion of the rehabilitation program can remove the default status from your credit report and restore your eligibility for benefits like deferment, forbearance, and loan forgiveness.

Settlement

Settlement, on the other hand, allows you to negotiate a reduced payoff amount with your lender. While it can provide immediate relief, settlement may have a negative impact on your credit score and may result in taxable income. However, it can help you avoid bankruptcy and achieve financial stability.

Assessing Financial Hardship

When pursuing a student loan settlement, it is crucial to demonstrate your financial hardship effectively. Here are some steps to help you assess your financial situation and gather the necessary documentation:

1. Calculate Your Debt-to-Income Ratio

Calculate your debt-to-income ratio by dividing your total monthly debt payments by your monthly gross income. This will give you an idea of whether you are in a financially distressed situation.

2. Gather Financial Documentation

Gather supporting documentation that demonstrates your financial hardship. This may include bank statements, pay stubs, tax returns, medical bills, or any other evidence that supports your claim.

3. Prepare a Hardship Letter

Write a detailed hardship letter explaining your financial situation, the reasons for your inability to repay the loan, and your request for a settlement. Be honest and provide as much information as possible to help your lenders understand your circumstances.

4. Consult with a Financial Advisor

Consider seeking guidance from a financial advisor or credit counselor who specializes in student loans. They can help you assessyour financial situation objectively, provide personalized advice, and assist you in navigating the student loan settlement process.

Working with Debt Settlement Companies

Debt settlement companies can assist borrowers in negotiating settlements with their lenders. However, it's important to approach this option with caution. Here are some key considerations:

Choosing a Reputable Debt Settlement Company

Research and select a reputable debt settlement company to ensure you receive reliable assistance. Look for companies with a proven track record, positive customer reviews, and transparent fee structures. Avoid companies that make unrealistic promises or charge excessive upfront fees.

Understanding the Fees

Debt settlement companies typically charge fees for their services. These fees can be based on a percentage of the total debt, a percentage of the amount saved through settlement, or a flat fee. Make sure you understand the fee structure and compare it with other companies to ensure you're getting a fair deal.

Evaluating the Benefits and Risks

Consider the potential benefits and risks of working with a debt settlement company. While they can negotiate on your behalf and handle communication with lenders, there's no guarantee of a successful settlement. Additionally, working with a debt settlement company may have a negative impact on your credit score and could result in legal action from lenders.

Reviewing the Settlement Agreement

Before signing any settlement agreement, carefully review the terms and conditions. Ensure that all the details, including the reduced payoff amount, payment terms, and any potential consequences, are clearly outlined. Seek legal advice if necessary to fully understand the implications of the agreement.

Tax Implications of Student Loan Settlement

When settling your student loans, it's essential to understand the potential tax implications. Here's what you need to know:

Forgiven Debt as Taxable Income

Under current tax laws, the forgiven portion of a debt settlement is generally considered taxable income. This means that you may be required to report the forgiven amount on your tax return for the year in which the settlement occurred.

Form 1099-C

If your lender forgives $600 or more of your debt, they are required to issue a Form 1099-C, "Cancellation of Debt," to both you and the IRS. This form reports the amount of forgiven debt, which you must include when filing your taxes.

Exceptions to Taxable Income

There are certain exceptions to the general rule of forgiven debt being taxable income. For example, if you can prove that you were insolvent at the time of the settlement, meaning your total debts exceeded your total assets, you may be able to exclude the forgiven amount from taxable income.

Seeking Professional Tax Advice

Given the complexities of tax laws and individual circumstances, it's advisable to consult with a tax professional when dealing with the tax implications of a student loan settlement. They can guide you through the process, help you understand your options, and ensure that you comply with all applicable tax regulations.

Rebuilding Your Credit After Settlement

While settling your student loans may have a negative impact on your credit score, there are steps you can take to rebuild your credit over time. Here are some strategies to consider:

Create a Budget

Develop a realistic budget that allows you to meet all your financial obligations, including any remaining debts, on time. Stick to this budget and avoid taking on new debts unless absolutely necessary.

Make Timely Payments

Ensure that you make all your payments, including credit card bills, utility bills, and any remaining debts, on time. Consistently making timely payments will demonstrate financial responsibility and help improve your creditworthiness.

Monitor Your Credit Report

Regularly check your credit report to identify any errors or discrepancies that could be negatively affecting your credit score. Dispute any inaccuracies and work towards resolving any outstanding issues promptly.

Apply for a Secured Credit Card

Consider applying for a secured credit card, which requires a security deposit and can help you rebuild credit. Use the card responsibly by making small purchases and paying off the balance in full each month.

Seek Professional Guidance

If you're struggling to rebuild your credit after a student loan settlement, consider consulting with a credit counselor or financial advisor. They can provide personalized guidance, help you develop a plan, and offer strategies to improve your credit score over time.

Seeking Professional Advice

When navigating the complexities of student loan settlement, it's highly beneficial to seek professional advice. Financial advisors, credit counselors, and legal experts can provide valuable insights and guidance tailored to your specific situation. Here's why professional advice is crucial:

Expert Knowledge and Experience

Professionals who specialize in student loan settlement have extensive knowledge and experience in dealing with lenders, negotiating settlements, and understanding the legal and financial implications. They can provide you with accurate information and guide you towards the best course of action.

Personalized Assessment

By consulting with a professional, you'll receive a personalized assessment of your financial situation and options. They can analyze your specific circumstances, help you understand the potential consequences of settlement, and provide advice based on your unique needs and goals.

Negotiation Support

Professionals can act as intermediaries and negotiate with lenders on your behalf. They have the skills and expertise to present a strong case, potentially increasing the likelihood of a favorable settlement agreement.

Legal Protection

If you're facing legal challenges related to your student loans, seeking legal advice is crucial. An attorney specializing in student loan debt can provide legal protection, ensure your rights are upheld, and represent your interests throughout the settlement process.

In conclusion, settling student loans can offer relief to borrowers facing financial hardship. By understanding the settlement process, exploring loan forgiveness programs, and seeking professional advice, you can make an informed decision that aligns with your financial goals. Remember, each individual's situation is unique, so it's important to carefully consider your options and choose the path that best suits your needs. With perseverance and the right strategies, you can overcome the burden of student loans and achieve financial freedom.

Comments

Post a Comment